It’s 2017 and one thing’s for sure: Businesses are growing internationally. Franchises are opening more and more locations overseas. Companies that sell online are extending their reach into new and often emerging markets.

While profitable for many, these types of expansions can be complicated, particularly when it comes to payment processing. Each region has its own unique payments landscape which must be considered prior to market entry.

We’ll get into specific scenarios, such as online retailers, a little later, but for now, let’s consider those factors that affect all merchants wishing to sell to international customers.

Platform Payment Integration

Whether your sales are initiated via a traditional ecommerce platform, your own website, or a third-party POS platform, the platform itself will need to be integrated with a payment processor that is registered to accept and process payments in the countries where you wish to expand.

One challenge many companies encounter: very few payment gateways can facilitate payments in every country where they wish to expand their business. Without this ability, businesses wishing to acquire customers globally will face increased cost and reduced speed to market related to integration of their platform with several unique payment channels.

One challenge many companies encounter: very few payment gateways can facilitate payments in every country where they wish to expand their business. Without this ability, businesses wishing to acquire customers globally will face increased cost and reduced speed to market related to integration of their platform with several unique payment channels.

This challenge was the inspiration that drove Constellation Payments to design a gateway where merchants connect to multiple processors while simultaneously benefitting from one provider for the bulk of their international transactions.

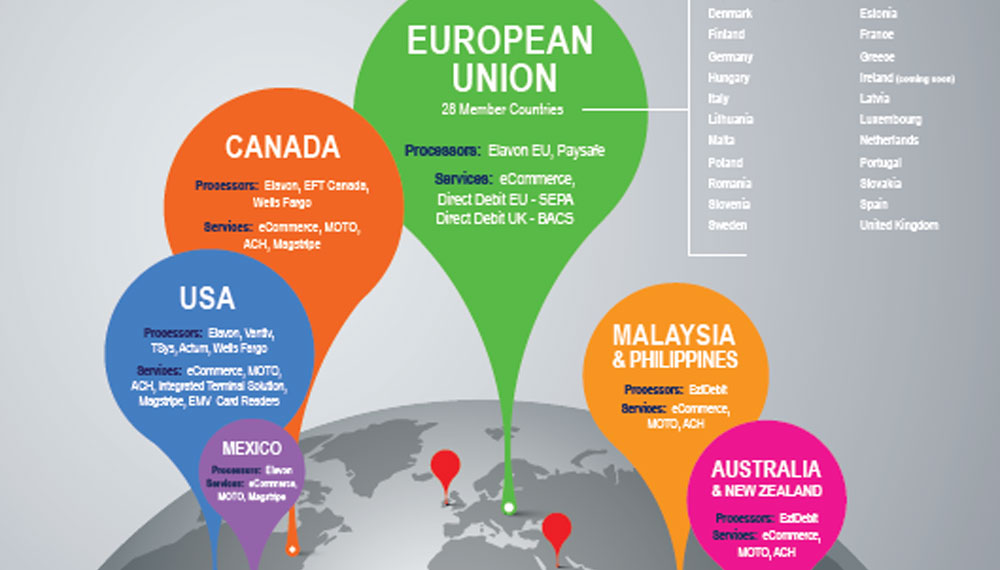

The Constellation Payments gateway can facilitate transactions in North America, Central America, United Kingdom, European Union, Australia, New Zealand, and multiple countries in the Asia Pacific region. Businesses wishing to accept payments from customers all over the globe should examine their current gateway’s capabilities to be sure it will match their expansion goals.

Research and Adapt

Not all markets function the same. For example, in Europe, consumer use of direct debit payment methods both for one-time and recurring transactions is far more prevalent than it is in North America or Asia. Companies that don’t understand this nuance will exclude themselves from a significant portion of the market. While you don’t have to offer every payment method under the sun, it is advisable to choose a platform/gateway combination that will offer the payment methods your target customer is most likely to use. When entering new markets, businesses are encouraged to discover what those methods are and evaluate their payment gateway and/or processor accordingly.

Another best practice is to present yourself and your company in the best possible light to foreign customers. Imagine tracking down a retail item you want to purchase only to discover that the site where you will purchase item is in a language completely foreign to you and in a currency different than your own. You can’t read the site, and you’ll likely have to leave the site and find an online currency conversion tool to verify that the price you are paying is acceptable.

Many customers facing this dilemma would simply leave the site without putting anything in their carts at all. Those that do proceed to checkout are likely to leave the site without completing their purchase due to the foreign currency issue.

In fact, 13% of all cart abandonment in 2016 was due to prices being presented in a foreign currency.

This is something we addressed at Constellation Payments early on. Our merchants can accept payments in the local currency of their customers no matter where they are, but still have the funds settled into their merchant accounts in their own native currency. This is all accomplished through something called Dynamic Currency Conversion (DCC).

Not all gateway and merchant services providers can provide this service though. It is highly recommended that companies going international verify whether DCC is available on their current platform and/or gateway configuration.

All this said, having localized versions of your website that acknowledge the language, customs, and currency of your target customer is highly advised when expanding internationally.

Clear Communication

In addition to the language and currency issues described above, it is also important that international customers purchasing physical goods understand any additional costs associated with purchasing from an overseas vendor.

When done right this is not a barrier to the sale at all. In fact, it is quite the opposite and somewhat expected. Clearly stating shipping costs, and making it easy to track items during the journey overseas, is critical. If there are duties or taxes that will be levied on foreign shipments, businesses will need to decide whether to absorb those costs or pass them on to the customer. If passing them to the customer, it should be crystal clear prior to finalizing the purchase.

B2B Challenges

There are some international challenges that are unique to the B2B world. For example, a company selling point of sale software will need to consider which foreign processors their merchants will be comfortable using and how their software users will obtain merchant accounts locally.

If a company in Mexico purchases the POS platform, not only will they want the POS platform to communicate in their native language, but when they have questions about things like deposits or chargebacks, they’ll want to speak with a payments professional that can speak their native language.

To address this for our own merchants, Constellation Payments has made strategic partnerships with carefully chosen local providers of merchant services, so that software companies connected to our gateway can refer their users to a local provider of payment processing that has been approved to process through our gateway and who understands local customs and banking regulations. These representatives can assist new merchants in applying for, using, and inquiring about their merchant accounts all in their native tongue.

Data Security

Another key issue when conducting transactions with foreign customers over the Internet is data security. Don’t let your company join the ranks of those with highly-publicized data breaches that have cost them billions in damages and lost credibility in the marketplace.

Constellation Payments is PCI-DSS Level 1 compliant, which is the highest level of certification available from the major card brands. Constellation also employs data encryption and credit card tokenization. Tokenization is the encoding of cardholder data such that it cannot be decoded without a key available only to the processor, and cannot be decoded or reused if intercepted by a third party.

Final Thoughts

Whether you are already offering your products or services internationally, or considering doing so, the team at Constellation Payments would be happy to review your processing needs and advise you as to your best options regarding payment processing.

Going Global: How to Successfully Sell Your Software Internationally

Going Global: How to Successfully Sell Your Software Internationally